For decades, Canada’s investment landscape was defined by a simple idea: Canadian capital should stay in Canada. It was an idea backed by regulations meant to keep investment at home – and one pension funds and other large institutional investors worried restricted their ability to maximize returns.

In fact, once the Foreign Property Rule was removed, investments flooded out of Canada, in a move that both the government and capital markets are looking to redress as growing tensions with the U.S. have them thinking about how to shore up the domestic economy.

Foreign Property Rule

The Foreign Property Rule was a regulation within the Canadian Income Tax Act that capped the amount of foreign assets which could be held in tax-deferred retirement accounts such as Registered Retirement Savings Plans (RRSPs) and Registered Pension Plans (RPPs). It was meant to ensure Canadian savings were used primarily to fund Canadian businesses and government debt, supporting the domestic economy. When it was introduced in 1971 it capped foreign investments at 10 per cent, but that number got as high as 30 per cent before the rule was abolished in 2005.

Foreign property rule limits

| Period | Foreign Property Limit |

| 1971 | 10% |

| 1990-1994 | The limit was raised incrementally by 2% per year up to 20% due to globalization and investor pressure |

| 1994 | 25% |

| 2001 | 30% |

| 2005 | Rule removed |

Any pension fund or institution that went over the limit faced a penalty, but there were also incentives for those that invested domestically. It was a way to reduce Canada’s economic dependence on the United States and prevent foreign takeovers of domestic industries.

This made sense when the economy was doing well, but when it faltered, individual investors worried that both their jobs and investments could be put at risk.

Institutional investors

When the 30 per cent cap was removed in 2025, institutional investors jumped on the opportunity to diversify abroad and invested heavily outside of Canada.

They argued that this allowed them to reduce concentration risk, since the Canadian stock market was small, representing just over three percent of the world’s capital markets. It’s also heavily concentrated on financials and energy. International investment provided diversification into sectors such as technology and healthcare, and access to higher growth markets with better protection against economic downturns.

In recent years, the S&P/TSX has outperformed the S&P500. For example, in 2025 the S&P/TSX Composite Index closed with returns of 28 per cent compared to the S&P 500 returns at around 18 per cent – but investment in Canadian capital markets was still slow to return.

Pension funds

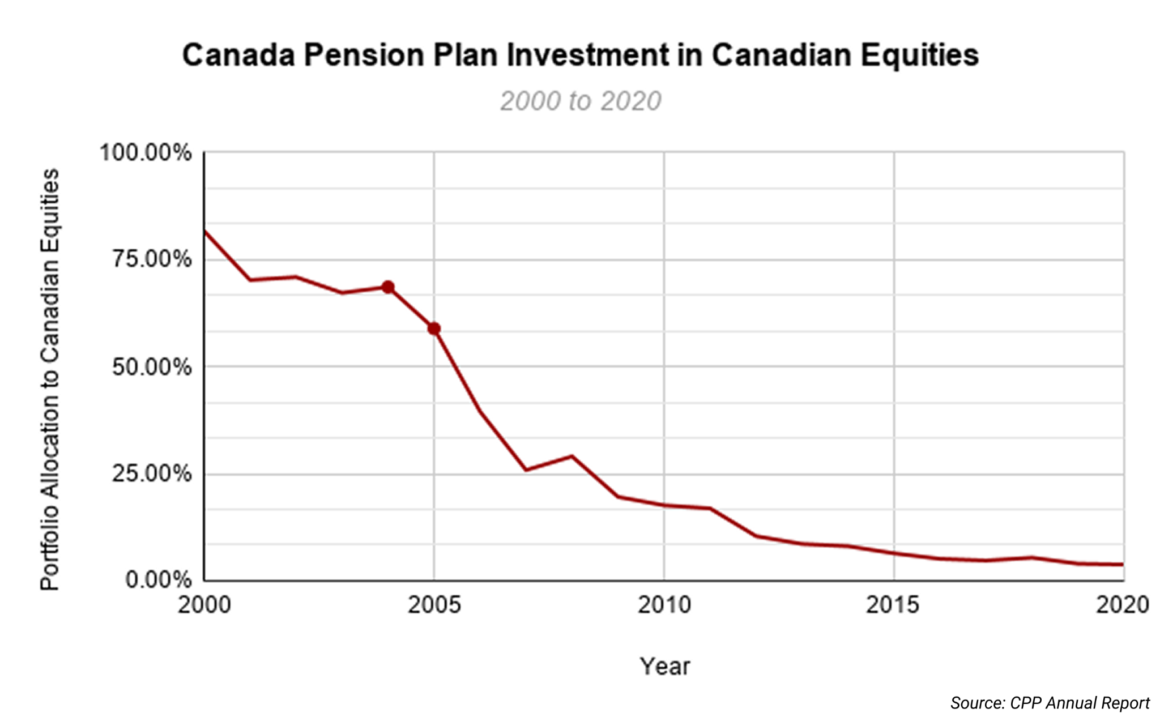

Pension funds were among the first to move their investments away from Canadian equities once the cap was removed. The Canada Pension Plan’s historical investment data shows the CPP’s allocation to Canadian equities dropped to 59 per cent in 2005 from 70 per cent in 2004. By 2020, their allocation was down to four per cent.

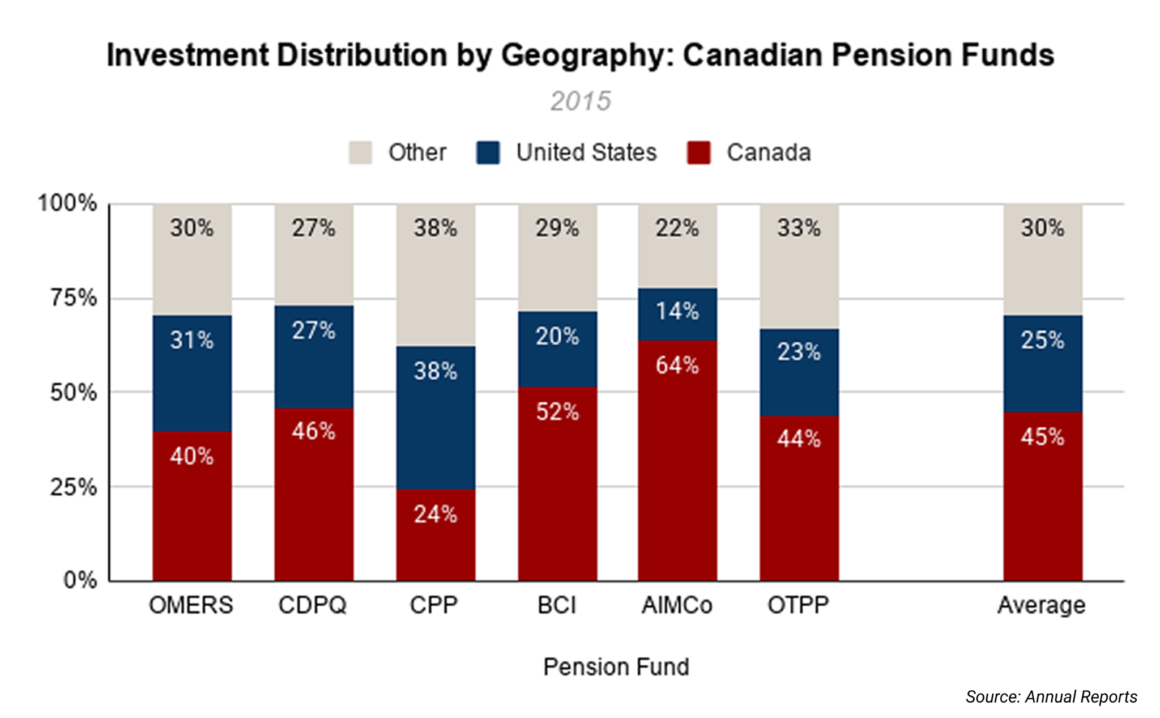

The shift away from domestic investment was not limited to CPP. Pension funds had historically maintained a strong domestic bias. In 2015, six of the “Maple Eight” held 45 per cent allocation to Canadian assets on average, whereas those same pension funds hold a 29 per cent allocation in 2025.

University endowments

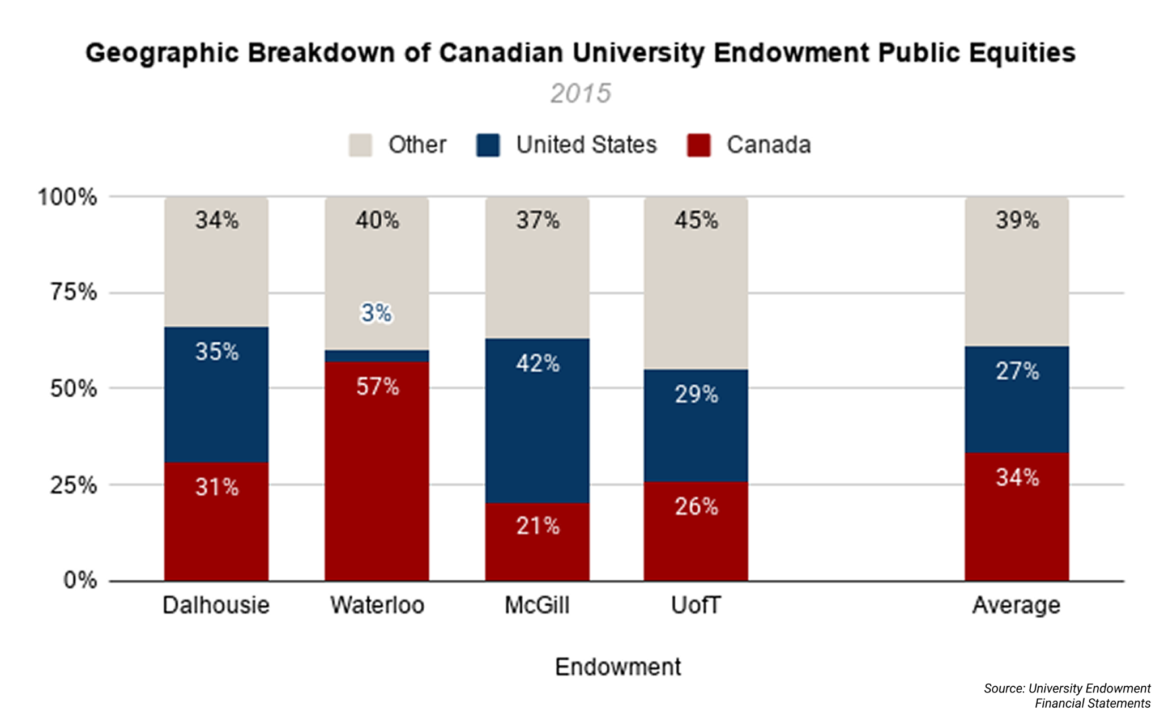

The same pattern applied to university endowments. In 2015, Canadian university endowments allocated roughly 34 per cent of their public equities to Canadian markets. In 2025, that figure fell to 16 per cent, an 18-percentage point decrease.

Across both pensions and endowments, the trend was consistent: As constraints were removed and global opportunities expanded, capital increasingly moved abroad.

Retail investors

Canadian retail investors have typically exhibited a strong home bias, and their concentration of domestic enquiries remained high even after the Foreign Property Rule was removed. In 2012, estimates suggested that Canadian retail investors held around 67 per cent of their exposure in domestic markets.

By 2024, Canadian exposure in retail portfolios had fallen closer to 56 per cent, an 11 percentage point decrease, reflecting a growing adoption of international mutual funds and ETFs, and investors increasingly allocating capital toward U.S. and global equities.

It’s a shift that was driven by structural changes to capital markets, such as the rise of low-cost ETFs providing easy access to global markets, increased awareness of sector concentration in Canada, and strong performance and growth of U.S. equities.

Attempts to keep capital in Canada

Poloz Initiative

After the institutional investor pendulum swung away from Canada, the federal government began looking at partial reversals of the Foreign Property Rule. In 2024, the Poloz Initiative was introduced to encourage Canada’s pension funds to increase their domestic investments. It focused on removing regulatory barriers and creating attractive investment environments rather than forcing domestic investment through punitive rules.

It also lowered ownership thresholds for municipal utilities, making it easier for pension funds to buy in and fund the Canadian electricity grid and required large pension plans to publicly disclose where their money is invested. It included a $1 billion fund for mid-sized companies and a $1 billion Venture Capital round being launched with favorable terms to lure institutional capital back into Canadian startups.

Sovereign Wealth Fund

In 2026, Prime Minister Mark Carney announced the Canada Strong Fund, a sovereign wealth fund meant to support national projects for the government in connection with both individual investors and the private sector.

These incentives are meant to bring Canadian capital back into Canada, by providing incentives to keep more money at home. Lower domestic investment can lead to slower productivity growth, fewer large-scale Canadian companies, increased reliance on foreign capital, and a potential hollowing out of capital markets.

Experts say collaboration between government and the private sector are key to get the right mix of investment back in Canada, and a look at both the history and current challenges around encouraging domestic investment show how crucial it is to get it right.