If you have any type of financing extended to you, such as a credit card, car loan, student loan, or mortgage, then you likely have a credit score.

In Canada, credit scores range from 300 to 900. This three-digit number tells lenders how well you manage credit and assesses the risk of lending you money. Your score is calculated using a formula based on your credit report, and there are many things that can either negatively or positively affect your score.

What does your credit score impact?

Having a bad or non-existent credit score can significantly impact almost every aspect of your financial life, making it difficult to obtain certain services or resulting in significantly higher costs to do so. Those include:

- Renting or buying an apartment

- Applying for insurance

- Getting any sort of financing, whether that be for a mortgage, credit card, car loan, education, etc.

- Some employment opportunities

- Security deposits

- Utilities and services

- Starting a business

What’s a good credit score?

Credit scores in Canada range from 300 to 900 and are divided into five tiers.

| What does that mean? | Percentile | Score |

| Excellent You’re a low-risk borrower and will have no problem borrowing money or obtaining any item mentioned above | 81 – 100% | 833 – 900 |

| Very Good Demonstrated in the past that you are reliable, and you will probably be approved | 61 – 80% | 790 – 832 |

| Good You’re a reasonable risk and will probably get approved | 41 – 60% | 743 – 789 |

| Fair You’re a higher risk borrower and will probably encounter trouble borrowing | 21- 40% | 693 – 742 |

| Poor Most likely will be denied for any of the items mentioned above | 1 – 20% | 300 – 692 |

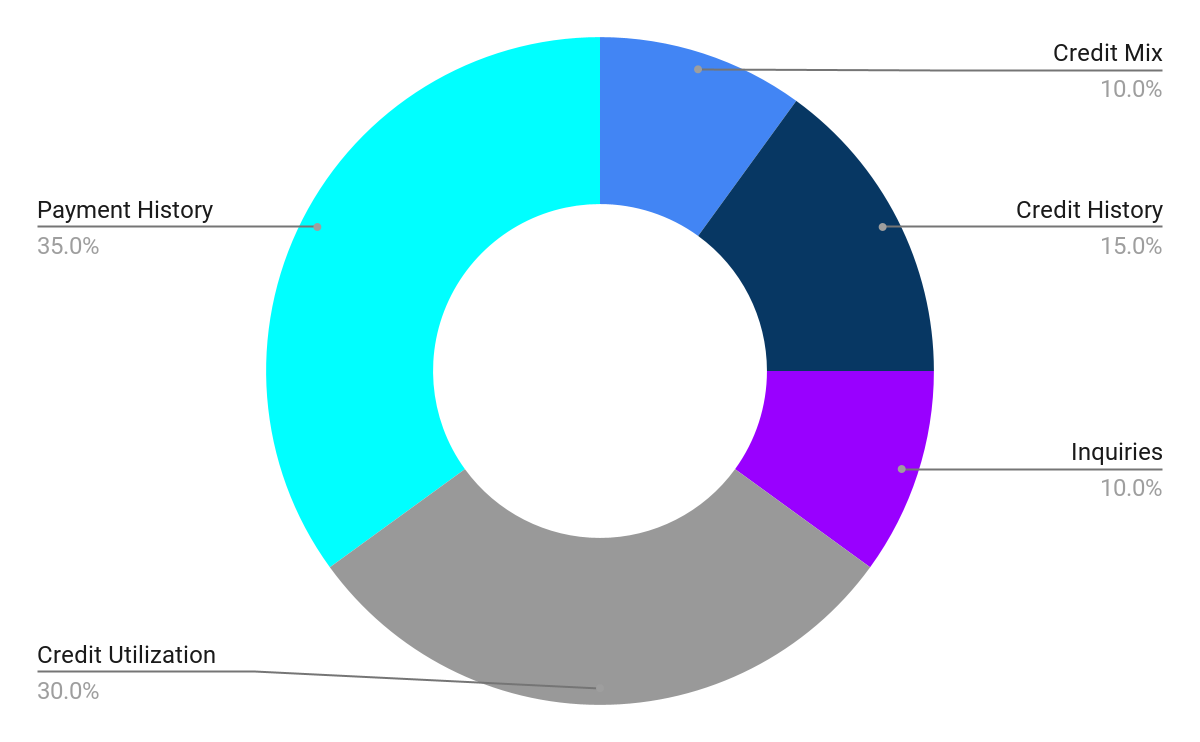

What impacts your credit score?

There are five categories that impact/make up your credit score:

Payment history has the biggest impact on your credit score because it indicates to lenders your ability and reliability to repay your debts. A history of on-time payments reassures lenders that you are a safer bet than someone who only pays on time 10% of the time.

- A single missed payment can bring an excellent credit score down as much as 63 to 83 points, whereas if you have a fair credit score, it’ll drop anywhere from 17 to 37 points.

- A missed payment stays on your credit report for seven years and generally takes three to five months of timely payments to start seeing improvements in your score.

Credit utilization is the ratio of your used credit to your available credit. This shows lenders how well you manage your current debt and your borrowing habits. If you spend the entirety of your available credit every month (high utilization), then it shows lenders that there’s a good chance you’ll run out of your ability to make your payments since you’re using so much credit. The lower your credit utilization score, the better, as it shows lenders that you use credit responsibly and are not overly reliant on it.

- To calculate it, divide your total credit card balance by your total credit limit. If you have a credit card with a $10,000 limit and typically use $1,000, your credit utilization would be 10%.

- You want to try to keep this at or below 30%. However, if you can get it below 10%, that would be golden.

- A high utilization score can impact your score by as much as 50 points.

When it comes to credit history, the longer you have had your credit accounts open, the better. Lenders prefer borrowers with long credit histories as it provides a longer track record of how you manage credit, which helps them assess the risk of lending to you.

- Your credit history is calculated by the age of your oldest account, the age of your newest account, and the average age of all your accounts. When you close an old credit card, especially one that has been open for a long time, it can reduce the average age of your accounts (and credit utilization), which can lower your credit score.

- The longer you have had the credit account open, the more it’ll improve your score.

- Keep in mind that some banks will deactivate the card after a prolonged time of no usage, so make sure to make a purchase on there every now and again.

Credit mix refers to the types of credit accounts you have open, whether that be credit cards, loans or mortgages. Lenders like to see that you’re able to manage different types of credit responsibility over a period of time.

Inquiries are for when anyone looks into your credit information, whether that be you applying for a new credit card, applying for loans, mortgages, or any credit at all, your credit will be checked through a process called a “hard inquiry” and in turn, it’ll knock off a few points from your score for about six months from the date of inquiry. Frequent hard inquiries can signal to lenders that you are actively seeking credit, which might indicate financial stress or risk of overextending your borrowing capacity.

- Even looking to see what your credit score is can sometimes be taken as a hard inquiry. So, make sure to check the fine print on websites or before doing any sort of financing to see if they’ll be doing a hard inquiry (impacts the score) or a soft inquiry (does not impact the score).

**Note that the higher your credit score, the greater the negative effects will be.

How to increase your credit score?

If you think your credit score is low, there are some ways that you can improve and maintain your credit score:

Always pay back your balance on time (or at least pay the minimum monthly rate). Avoid missing a payment on anything.

- Set up payment reminders on your phone, or you can set up auto deposits through your bank

- Nerdy tip: To make sure you never miss the minimum monthly payment, you could set up an auto deposit to have $10 (or whatever your minimum is) put towards your unpaid balance a week before your payment is due

Limit the number of credit cards you open. Every time you open up a new credit card, you’ll be subject to a “hard inquiry.”

Write a goodwill letter. Let’s say a missed payment but have a valid reason for doing so, (maybe you moved, were ill, lost your job, or were sick).

- A goodwill letter is a letter sent to a creditor (not a credit bureau) to explain a previous behaviour that negatively affects your credit rating.

- This could result in a late payment being removed from your credit report and could possibly increase your credit score up to 100 points within 30 days.

Keep your credit utilization score below 30% each month. The sweet spot is between 10% and 15%. To improve your credit utilization score, you can either:

- Pay off your existing debt.

- Ask for an increase to your credit limit.

- Apply for another credit card, which would also increase your available credit.

Don’t shut down your old credit cards unless you absolutely have to. Even if you don’t use it anymore, keep it open and use it every once in a while.

- Make sure to check your credit report monthly, there could be inaccuracies that you may be able to dispute and possibly boost your score if the errors are corrected.

Rent reporting services: Some services allow you to report your rent payments to credit bureaus, such as RentTrack or Rock the Score. This can help build your credit history if these payments aren’t traditionally reported.

Credit builder loans: Some Canadian financial institutions offer credit builder loans. These loans are designed for individuals with limited credit history or poor credit scores. The lender holds the loan amount in a savings account, and you make payments toward it. Once paid off, you receive the funds, and your positive payment history is reported to credit bureaus. This can also help your credit mix.

Become an authorized user: You can ask a family member or close friend with good credit to add you as an authorized user on one of their credit cards. This can help improve your credit score by potentially adding positive payment history, lowering your credit utilization ratio, diversifying your credit mix, and increasing the average age of your credit accounts.

Where can you see your credit score?

Canadians can use websites like Equifax and TransUnion to access their credit scores for free. Additionally, many banks provide credit score access directly through their mobile apps. But always check whether the inquiry will affect your credit score. Also, beware when using services to check your score because some may have hidden fees, so always make sure to read the fine print.

Nerdy Tip: If you have a BMO credit card or access your credit report through TransUnion, you can use their credit score simulator to see how various scenarios, such as adding a new line of credit or missing a payment, might impact your credit score.