Getting your first credit card can feel a bit like winning the lottery – all this credit to spend, no matter how much money you have in the bank. But credit isn’t money – and mismanaging a credit card can lead to a bad credit score, which can have a huge impact on the rest of your financial life. It can take months or even years to reverse the negative effects of a bad credit score – so it’s crucial to understand how credit cards work – and how to use them to build credit, not lose credibility.

Using a credit card

Most people have two main types of bank cards: credit cards and debit cards. When you make a purchase with a debit card, money is pulled straight out of your bank account, so you can only spend the amount in your account (plus anything allowed on overdraft, if you have that feature).

With a credit card, you can spend up to a specified amount set by your bank (credit limit) and pay it off later – regardless of how much cash on hand you actually have.

Don’t get too excited about the “later,” thought. It doesn’t mean you can spend your entire monthly limit and use it as “free money” that you can pay back whenever you want. That’s exactly the type of mindset that will royally mess you up financially in the future.

Your credit limit is the maximum amount you can borrow/spend from the bank, and you must repay the amount you spent monthly. Each month, you’ll receive a payment due date, which is the deadline to repay the used amount. You can find this date on your credit statement, which also includes the total amount you owe, shown as the balance due.

It’s important to pay the balance due amount on (or ideally before) the payment due date; otherwise, you’ll be charged interest (referred to as the APR or Annual Percentage Rate) on any outstanding unpaid balance. Most people run into trouble when they start to consistently carry an unpaid balance. That not only means they will end up owing more money for every month it’s left unpaid (due to interest), but also has negative consequences for credit scores.

Understanding credit card statements

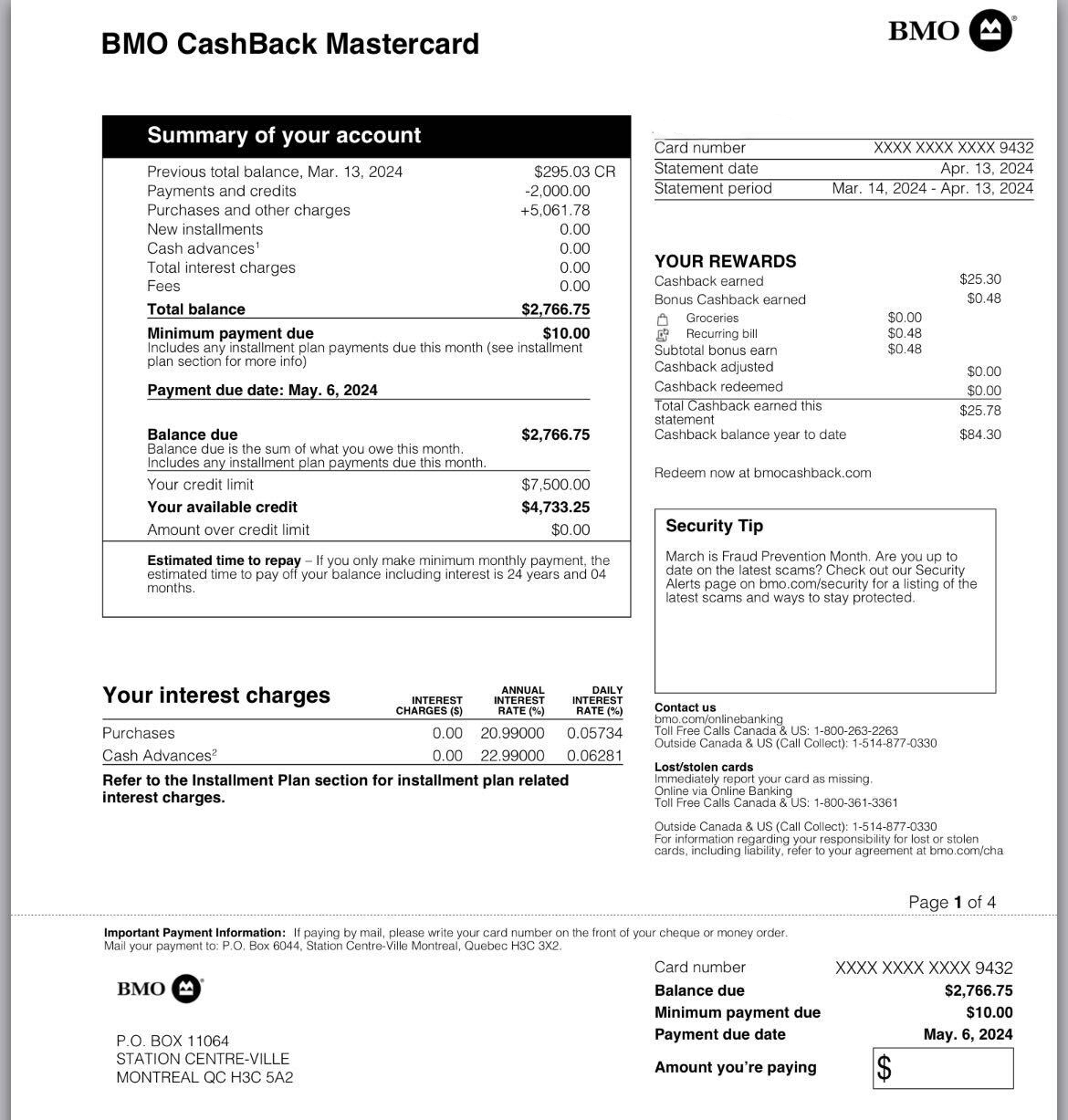

This is what your credit card statement will look like. You’ll receive it monthly, usually by mail, although you can opt to have them sent to you through email (e-statements), or opt out all together and just look at it online in your bank account. Your credit card statement shows a summary of all the transactions you made during the statement period, how much you owe, and the day you must pay it off by.

This is how it breaks down:

Balance due: This is how much you have outstanding as of the statement date, and how much you must pay back or you’ll be charged interest on it.

Payment due date: This is when you’re required to either pay the minimum or the full balance.

Statement date: This is when you received your credit statement.

Available credit: This is how much you can spend.

Annual interest rate (APR): Divide this by 12 to get your monthly rate and see how much interest you’ll have to pay on an outstanding balance.

Estimated time to repay: This shows you how long it would take to repay the full amount if you only payed the minimum each month.

Interest charges: This is how much you owe in interest on top of your unpaid balance.

Fees: Some cards have a monthly or annual fee in order to use the card and the card’s benefits. That amount will show up here along with any other fee you may have incurred, like overlimit fees, late payment fees, or cash advance fees.

What can you gather from this statement?

You must pay $2,766.75 by May 6th, otherwise you’ll owe $2,815.15 ($2,766.75 * (1+ (0.2099/12)) in next month’s statement. It would cost you approximately $48 extra if you missed or didn’t pay the balance by the 6th of May.

Paying your credit card

You can pay off your credit card either online (through the app or your bank’s website), by telephone, at an ATM, in person at a branch, by pre-authorized debit, or by mail with a check.

What happens if you can’t pay the full amount?

When it comes to your credit card, there are only three options regarding payment:

- You pay the full amount: This is ideal as you won’t owe any interest, and consistently paying the full amount will help maintain or improve your credit score.

- You pay the minimum amount (either $10 or the amount set by your bank): It won’t count as a late payment or hurt your credit score (in the short term), but you’ll be charged interest on the remaining unpaid balance. Consistently paying only the minimum can increase your credit utilization ratio, which might negatively impact your credit score over time.

- You don’t pay at all/miss the payment: You’d be charged interest on the outstanding balance, and if a payment falls 30 days or more past due, a delinquency is noted on your credit report, which will negatively impact your credit score and on top of the added interest, you could also be charged a late payment fee.

*Nerdy tip* ~ ALWAYS AT LEAST pay the minimum amount each month. It’s not a long-term solution, but it’ll save you from large hits to your credit score.

Let’s consider an example: Your APR is 22%, and your balance due on January’s statement is $1,000. If you don’t pay anything back by February’s payment due date, you’ll owe $1,018.33 [$1,000 * (1+ (0.22/12)]. Suppose you still haven’t paid that back by March’s payment due date. In that case, you’ll owe approximately $1,037 [$1,018.33 * (1+ (0.22/12)], and since it’s been over 30 days, it now counts as a late payment, and your credit score could drop as much as 83 points (depending on your current score).

If you just paid off the minimum each month, see how long it would take you to pay off your balance with our debt repayment calculator.

What happens if you exceed your credit limit?

While you are sometimes able to spend beyond your limit, you should try to avoid it. If you were to exceed your credit card limit, you face declined transactions, steep penalties, charged overlimit fees, a possible drop in your credit score — and the potential for your issuer to freeze or close accounts.

*Nerdy tip* ~ Beware of your available credit vs. credit limit. These are two different things. Your available credit is how much of your credit limit you have left to use and your credit limit is how much total you can spend each month.

To learn more about what all this can mean for your credit score, read this.