Anyone looking for a new mortgage in times of rising interest rates ought to pay attention to the yield curve and understand the relationship between bond yields and fixed mortgage interest rates.

Lenders peg fixed interest rates to bond rates, but variable rates aren’t affected in the same manner – it’s monetary policy decisions made by central bankers that most affect variable-rate loans that are tied to the prime rate.

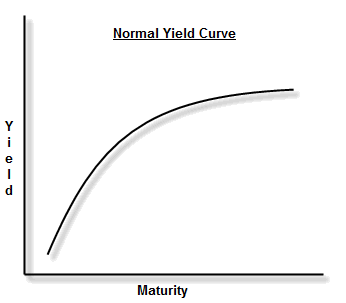

The yield curve plots interest rates and maturities for bonds of equal credit quality, with the years to maturity on the x-axis and the yield on the y-axis. Healthy economies generally have upward-sloping yield curves, also referred to as normal yield curves.

Bond prices and interest rates

There is an inverse relationship between bond prices and interest rates. Bond prices rise when interest rates go down and decline when interest rates go up. This is because as interest rates go up, any existing bonds are worth less in the secondary market.

Bond yields and mortgage rates

Mortgage lenders’ fixed interest rates are closely tied to bond rates. Low yields on government bonds mean low rates on fixed rate mortgages and vice versa. When bond yields decline, fixed mortgage rates also come down – a direct relationship.

Since bond prices and interest rates move in opposite directions, as bond prices go down, fixed mortgage rates go up and vice versa – an inverse relationship.

Correlation between fixed mortgage rates and bond yields

Fixed-rate mortgages are riskier assets for banks compared to government bonds, which are viewed as safer or risk free. This is because repayment is guaranteed with bonds issued by governments of developed democratic nations, but not with mortgages, whose repayments hinge on the financial well-being of individuals.

Mortgages present default and prepayment risk, which can alter the expected return on investment and timing of cash flows. Mortgage rates are higher than government bond rates to compensate for the additional risk.

How much higher are mortgage rates over bond rates?

Banks typically use 5-year bond yields to determine their fixed mortgage rates, taking the forecast earnings from bond investments to cover the costs and potential losses they might incur in the mortgage market.

As the 5-year bond yield rises, lenders’ margins will shrink and then ultimately disappear, as funding costs increase. When they can no longer absorb the increase it gets passed on to borrowers by way of higher fixed mortgage rates.

Banks don’t automatically raise fixed mortgage rates as bond yields increase, but when bond yields climb, fixed rates typically follow.

From 2020, the only way is up

Fixed mortgage rates in Canada and the U.S. dropped to historic lows in December 2020 as investors fled to the safety of government securities. They then bounced around during most of 2021 before shooting up in September of that year.

While 5-year mortgage rates are expected to remain low by historical standards, they are forecast to rise in 2022. Short-term variable interest rates are at their “lower bound” and not expected to fall any further.

For variable-rate mortgages, it’s the overnight lending rate, as set or influenced by central banks’ monetary policy rate-setting decisions, that has the greatest impact.

In the U.S. it’s called the Fed Funds Rate. This rate is what banks charge each other for overnight loans needed to maintain their reserve requirements. It influences LIBOR and prime rates, the key benchmarks used to price adjustable-rate loans like a variable-rate mortgage.

Watch bond yields to make mortgage decisions

The best time to get a fixed-rate home loan is when yields are low. By historical standards, they remain low at the time of writing in 2022, but with multiple rate increases expected over the next few years, bond yields – and fixed mortgage rates – look to be on the rise.