Why all the talk about mortgage payments, whenever the Bank of Canada makes a rate announcement? This is because anyone with a variable rate mortgage is affected by changes in short term interest rates. Variable rate mortgages are tied to the prime lending rate or prime rate, which is driven by the key policy rate set by the Bank of Canada. These are also known as short-term interest rates. Mortgagers secure a variable rate that is quoted as prime plus or minus a certain percent. This rate is used to calculate the interest on the mortgage and the payment amounts.

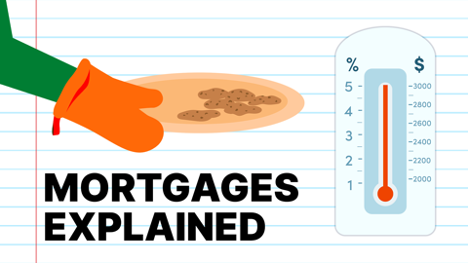

Our trusty FinPipe thermometer gives us a reading on just how much variable mortgage payments could rise if rates are going up like they are in 2022. See how when short term interest rates are on the rise, variable rate mortgage payments will go up too? To keep things simple, we used a brand new $500,000 mortgage with a 25 year amortization period and monthly payments to make these calculations. While one and a half percent to 5% is a big move for interest rates, the key policy rate in Canada is already up two and a quarter percent since March. The difference in those payment amounts is considerable, especially when so many households are already living paycheck to paycheck. And we have more rate announcements to come.

Anyone considering a variable rate mortgage ought to crunch the numbers to figure out how much their payments would change if interest rates were to increase or decrease. Although, the former is more important because having extra money isn’t exactly a problem that people need to budget for. Note that when the prime rate changes, you’ll get a notice from your mortgage company telling you your new payment amount. To learn more about variable versus fixed rate mortgages, check out the article links below.