Update: Canada’s Federal tax brackets and personal tax credit amounts will increase in 2025, reflecting a 2.7% inflation adjustment. This means more of your income remains in lower tax brackets, leaving you with more take-home pay compared to 2024.

Most people have experienced that sinking feeling when their paycheque is less than anticipated. Or the dismay at all the deductions on a pay stub. Employers are required to make these deductions, so people have to learn to live with them – and understanding what they mean may help to accept them.

Canada Revenue Agency (CRA) collects taxes and other payroll deductions from Canadians and distributes the funds to various government departments to help cover the cost of federal and provincial social programs that benefit individuals and communities.

Knowledge is key

Tax documents are loaded with acronyms and jargon, which definitely doesn’t help with understanding payroll deductions or being able to tell if pay stubs are accurate.

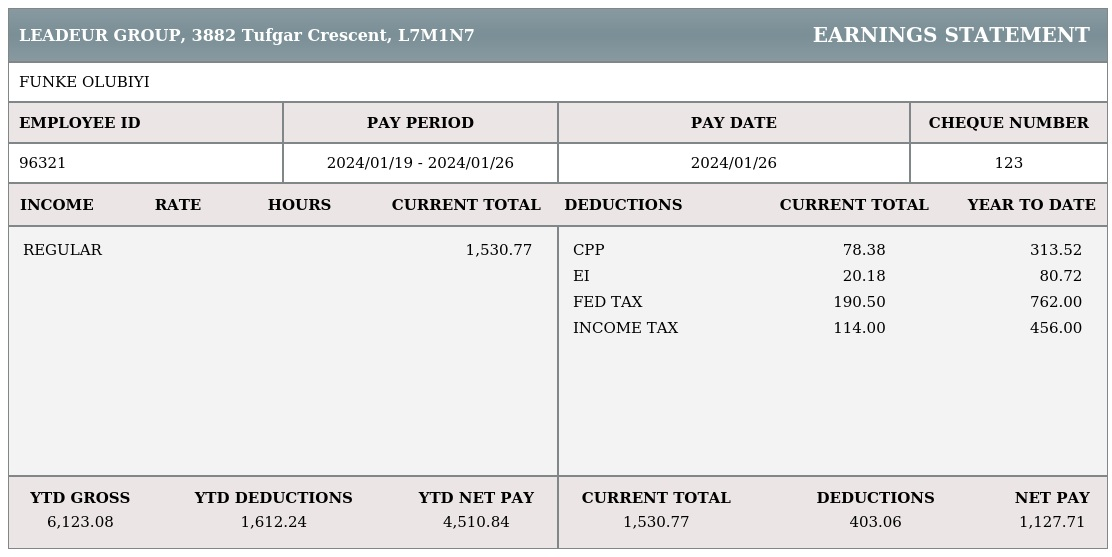

A pay stub shows an employee’s income and any payroll deductions, like income tax, Employment insurance (EI), and Canada Pension Plan or Quebec Pension Plan (CPP/QPP), as well as take-home pay. Its name comes from the fact that it used to be attached to a paper paycheque, which could be removed for filing — a “stub.”

A summer 2022 survey by Payments Canada revealed some interesting findings about Canadians:

- 57% don’t pay attention to the income and deduction amounts on pay stubs.

- 47% pay more attention to social media than their pay stubs.

- 35% find reviewing their payment information intimidating.

- 35% don’t fully understand all the details on their pay stubs, but assume they are correct.

According to Kristina Logue, Chief Financial Officer of Payments Canada, “many Canadians are silently struggling to decipher their pay details and are taking a ‘hope for the best’ approach to accuracy.”

This needs to change because understanding paycheques and knowing how to read pay stubs is an important component of financial literacy and essential for financial well-being.

Source: https://www.canadapaystubs.com

Everyone should periodically review their pay stubs – especially at the start of a new year and whenever the take-home pay amount changes (which doesn’t necessarily mean there’s a problem, but it’s worth checking to be sure there isn’t).

Federal and provincial income tax

How much you pay in income taxes is heavily influenced by how much you make, since Canada employs a progressive tax system, where higher income equals a higher income tax rate.

The federal government determines federal income tax rates while each province and territory decides their own rate, which applies in addition to the federal one.

Employers are required to make regular tax deductions. Federal and provincial income tax is deducted from paycheques, preventing people from getting a huge tax bill — and potentially being unable to pay it on time or at all. While payroll deductions aren’t popular, they’re a fact of working life.

Employers estimate what each employee will owe in taxes using TD1 forms that show the federal and provincial/territorial deductions being claimed by employees. It’s an estimate and tends to be less accurate for people with more and/or larger tax deductions.

If too much income tax gets deducted, the balance is refunded to the employee when they file their tax return. The opposite happens if not enough taxes were deducted, which means there will be a tax balance owing at the time of filing.

Brackets and rates

Canada’s progressive tax system applies higher tax rates to higher ranges of income, also referred to as a tiered multiple-rate system. The highest-tier rate that applies to a taxpayer’s income is their marginal tax rate, but the marginal tax rate doesn’t apply to one’s entire income.

Income tax is based on tax brackets, which are different ranges of income. Taxpayers can have income that spans multiple tax brackets and each tranche is taxed at the rate for that tier or range. For example, someone who earns $50,000 will be taxed at one federal rate (15%) while someone who earns $250,000 will be taxed at all five federal rates (15% on the first $55,867, followed by 20.5% on anything between $55,867.01 and $111,733, and so on). The tax brackets are indexed to inflation, based on the Consumer Price Index (CPI), and adjusted annually.

Income is segmented across the brackets, each with its own tax rate, at the federal and provincial levels. Canada has five different federal brackets, which are shown below. The number of provincial and territorial brackets ranges from as few as three in Manitoba and Saskatchewan to as many as eight in Newfoundland and Labrador.

The average tax rate is the overall percentage an individual pays, based on multiplying their income by the rate for each bracket that applies. The average rate a taxpayer pays is referred to as their effective tax rate.

This would be the effective tax rate on a $75,000 income:

The last time the federal rates changed was when the government switched from four brackets to five for the 2016 tax year, which saw them change the rate for the second bracket and introduce a higher one for the new fifth bracket.

Canada Pension Plan (CPP & CPP2) and Quebec Pension Plan (QPP)

Participation in the Canada Pension Plan is mandatory, even for those with employer-sponsored pension plans. Quebec has its own government pension program. Anyone aged 18 to 70 years with annual income in excess of $3,500 must make CPP or QPP contributions.

CPP and QPP contributions are 5.95 per cent and 6.4 per cent of income, respectively, up to the 2024 maximum amounts of $3,867.50 for CPP and $4,160 for QPP. Employers are required to match employee CPP and QPP contributions. Self-employed individuals must make both employee and employer contributions, meaning they contribute double what employees do.

The government introduced a CPP enhancement in 2024. Second additional CPP contributions (CPP2) apply to income above $68,500 up to a ceiling of $73,200. Employees and employers must make CPP2 contributions at a four per cent rate, which equals a maximum of $188 in additional deductions (for 2024). Anyone who earns less than $68,500 won’t see any changes to their CPP contributions.

These monies are allocated to the relevant plan and gradually returned to taxpayers when they retire and draw on their government pension.

Did you know?

Income tax was first introduced in Canada in 1917, to help finance participation in World War I. Until that time Canada was a tax-free haven, which the government promoted to attract skilled immigrants and investors.

Employment Insurance (EI)

Employment insurance provides temporary income support to people who were laid off or are otherwise out of work, not by choice. Participation is mandatory, even for individuals who have never benefited from the program.

Employers must deduct EI premiums from all employees’ pay, regardless of age. There is no match required from those who are self employed.

Employee EI premiums are 1.66 per cent for 2024, up to a $1,049.12 maximum. Employers pay 1.4x the employee amount, up to a $1,468.77 maximum. Premiums are different in Quebec, as they administer their own employment insurance program.

A couple points about maximums

First, the federal government sets maximum amounts each year for CPP, QPP and EI.

Given the limits on these deductions, some individuals will reach the maximums before the year is over, at which point their paycheques will go up for the remainder of that year. Those deductions will stop appearing on their pay stub and then everything resets on January 1st.

Ask for help

Personal income taxes and payroll deductions aren’t exactly straightforward, so it’s always a good idea to ask someone in the know. A good place to start would be your employer – specifically the payroll department. They should be able to assist with any inquiries about pay stub details and reviewing them in the event of any discrepancies. If still in doubt, consult a tax expert about any lingering questions or concerns.

Footnote:

Effective Tax Rate calculation is as follows:

[$55,867 * 0.15 + ($75,000-55,867) * 0.205] ÷ $75,000 = 16.40%