When interest rates are low on everything else, it’s hard to understand why credit card interest rates remain so high.

In the midst of the COVID-19 pandemic in 2020, with the prime rate in Canada hovering at or near a record low of 2.25%, the average interest rate on a Canadian credit card was still around 20%.

Americans were paying an average of 17% — above all other forms of debt, except maybe payday loans — with their prime rate at 3.25%.

The prime rate vs. credit card interest rates

The interest rate discrepancy is partly due to the fact that there’s no direct correlation between the prime rate and the interest rates charged on credit cards. According to the Canadian Bankers Association (CBA), the overnight lending rate set by the Bank of Canada generally does not influence consumer lending or credit card interest rates.

Most credit cards offer a fixed interest rate, meaning that there is a single, unchanging percentage. But, some are variable, with the rate tied to a financial index. So, when the index moves up or down, the card’s interest rate would adjust in tandem.

So what does affect credit card interest rates?

Collateral or secured lending

Secured lending rates are always lower than unsecured ones, on account of the borrower putting up assets as collateral against future debt. The lender has recourse to seize and sell the asset(s) to cover any outstanding debt, so there is less risk for the lender, which usually leads to a lower rate.

Think about mortgage rates, which are lower because your house is posted as collateral. If you fail to repay the outstanding balance on an unsecured credit card, it’s a lot more difficult for issuers to recover the funds. If you default or file for bankruptcy, the issuer will write off the loss.

Grace period

This is the interest-free period that applies on virtually every credit card, from date of purchase until payment, as long as the balance is paid in full by the due date. If you pay your balance in full every month, you’re essentially getting free short-term financing.

Transaction and technology costs

There are numerous costs associated with operating credit card systems, including processing transactions, statement preparation and distribution, as well as payment collection and reward programs.

What’s more, there are frequent technology upgrades and credit card issuers are always coming out with new card features and innovations — upgrades that issuers usually make cardholders pay for.

Fraud

It’s expensive to fight fraud and reimburse customers, since Canadians are not responsible for fraudulent charges. Financial institutions reimburse Canadian credit card customers hundreds of millions of dollars every year.

Most major U.S. credit cards have zero-liability protection, so the issuers are on the hook for these losses, which they pass on to consumers in the form of higher interest rates.

Legislating rates

In 2009, U.S. Congress passed the Credit Card Accountability, Responsibility, and Disclosure Act. Among other things, it limited the banks’ flexibility to raise interest rates for their credit card customers. Canada announced less extensive changes and measures later that year, which took effect in 2010.

The unintended consequence of these restrictions was that banks simply increased their introductory rates to a higher level than otherwise would’ve been the case. This explains at least some of the above-average increases in card rates after the 2008 financial crisis.

Comparing rates

Government bond yields are frequently quoted when referring to the general level of interest rates in Canada and the U.S. However, this refers to rates charged to the highest-quality borrowers,so it’s really not the most relevant comparison to personal credit card interest rates.

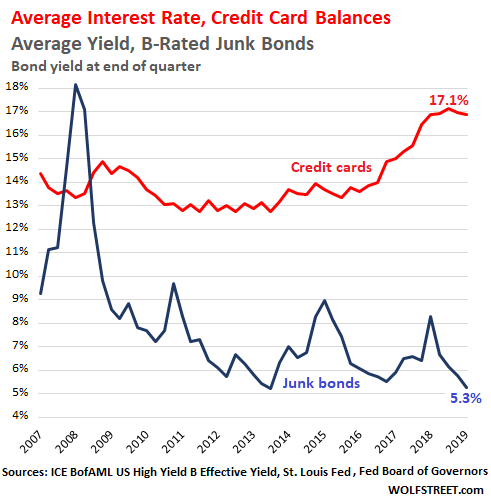

A more appropriate comparison is B-rated junk bond yields, which reflect the rates charged to higher-risk borrowers. You can see there is an upward trend for credit card interest rates going back to around 2013. And, the difference (or spread) between these rates has almost doubled over since 2010, from around 6% to nearly 12% at the end of 2019.

Credit Card Interest Rates vs. Junk Bond Yields (U.S.)

***Bond yields as of the end of each quarter.

There is a clear disconnect between the average B-rated junk bond yield (blue line) that plummeted to record lows and the rising average interest rate on credit cards (red line) that hit record highs of late. They should move roughly in the same direction with a gap between them, but they’ve actually been moving in the opposite direction since 2018.

So what are your options?

There isn’t a lot you can do to bring down the APR on your credit card, short of getting the most basic one and having the ability to secure it.

But if you control how you use that credit and make sure you pay your balance in full, you get that record low rate of 0% on all your purchases!